Clarwise

How Residual Load Shapes Electricity Market Price

Residual (demand - renewables) turns out to be a surprisingly informative lens for understanding Poland power prices from 2020 to 2025. A quick visual analysis before building quantitative models.

In this post we take a simple, practical look at how one metric – residual load – helps explain Poland’s power prices over the last few years.

No single variable tells the whole story in a market that has gone through a fuel crisis, fast renewables build‑out and regulatory changes. But residual load (demand minus renewables) turns out to be a useful starting point.

We focus on straightforward visuals: scatter plots of residual load versus market prices (PLN/MWh) from the Polish day‑ahead market, based on data published by PSE, year by year from 2020 to 2025. The goal is to see what we can already learn from the charts before moving on to more detailed “what‑if” analysis in the next step.

Residual load: a quick refresher

Residual load is the portion of demand that must be covered by dispatchable generators after subtracting variable renewables (mainly wind and solar):

Residual load = Total demand − Wind − Solar

Residual load is a very useful metric for understanding price formation. It directly links the merit order to prices: the higher the residual load, the more capacity has to be brought online, typically from more expensive plants. It also implicitly captures many structural changes in the system — renewables build‑out, demand trends, and changes in thermal fleet availability. And it is straightforward to use in “what‑if” terms: for example, we can ask what happens to prices if residual load is 2 GW lower because more PV is added to the system, or how prices respond when 1 GW of BESS shifts load and discharge across hours.

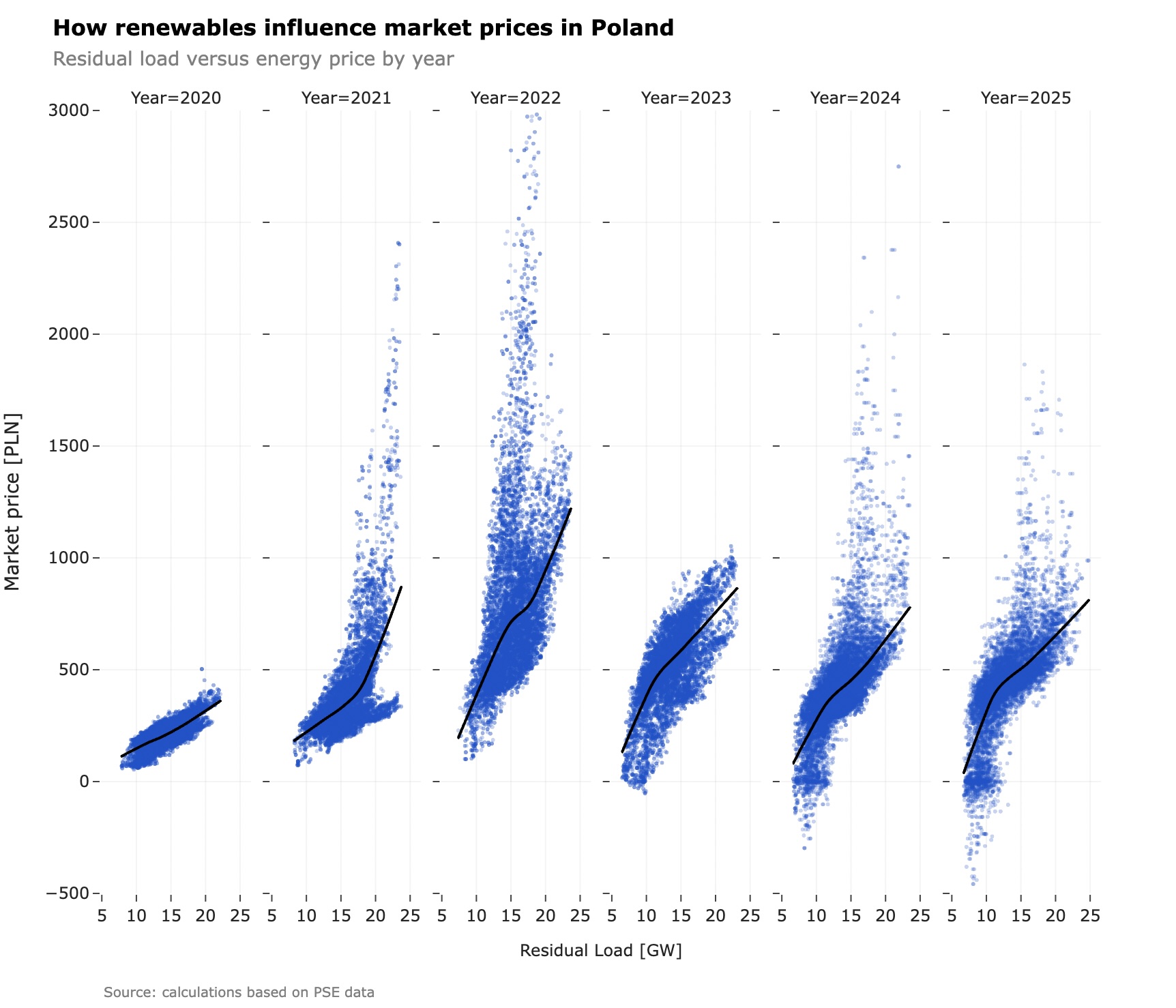

The chart: six years, one relationship

The figure above compares hourly market prices (PLN/MWh) against residual load (GW) for each year from 2020 to 2025. Each point is an hour; the black line is a smoothed trend for that year. Even without any modelling, the scatter already spells out how the merit order shows up in prices.

Across years, the whole curve shifts. For a given level of residual load, prices in 2021 and especially 2022 sit well above other years – the fuel crisis in picture form, as higher gas and coal prices plus high carbon costs lifted the entire merit order. From 2023 onwards the curves move back down: the same 15 GW of residual load that implied very high prices in 2022 corresponds to much more moderate prices by 2024–2025 as input costs ease and more renewables enter the system.

Another notable feature is how the shape of the curve evolves over time. In 2020 the dependency is relatively linear, with prices rising steadily as residual load increases. Years 2021 and 2022 show increasing curvature, with prices escalating more sharply at higher residual loads due to heightened fuel costs. The curve is convex – relatively flat at low residual loads and gets steeper as residual load increases, reflecting the growing impact of expensive peaking units during high demand periods. This is particularly evident in 2021.

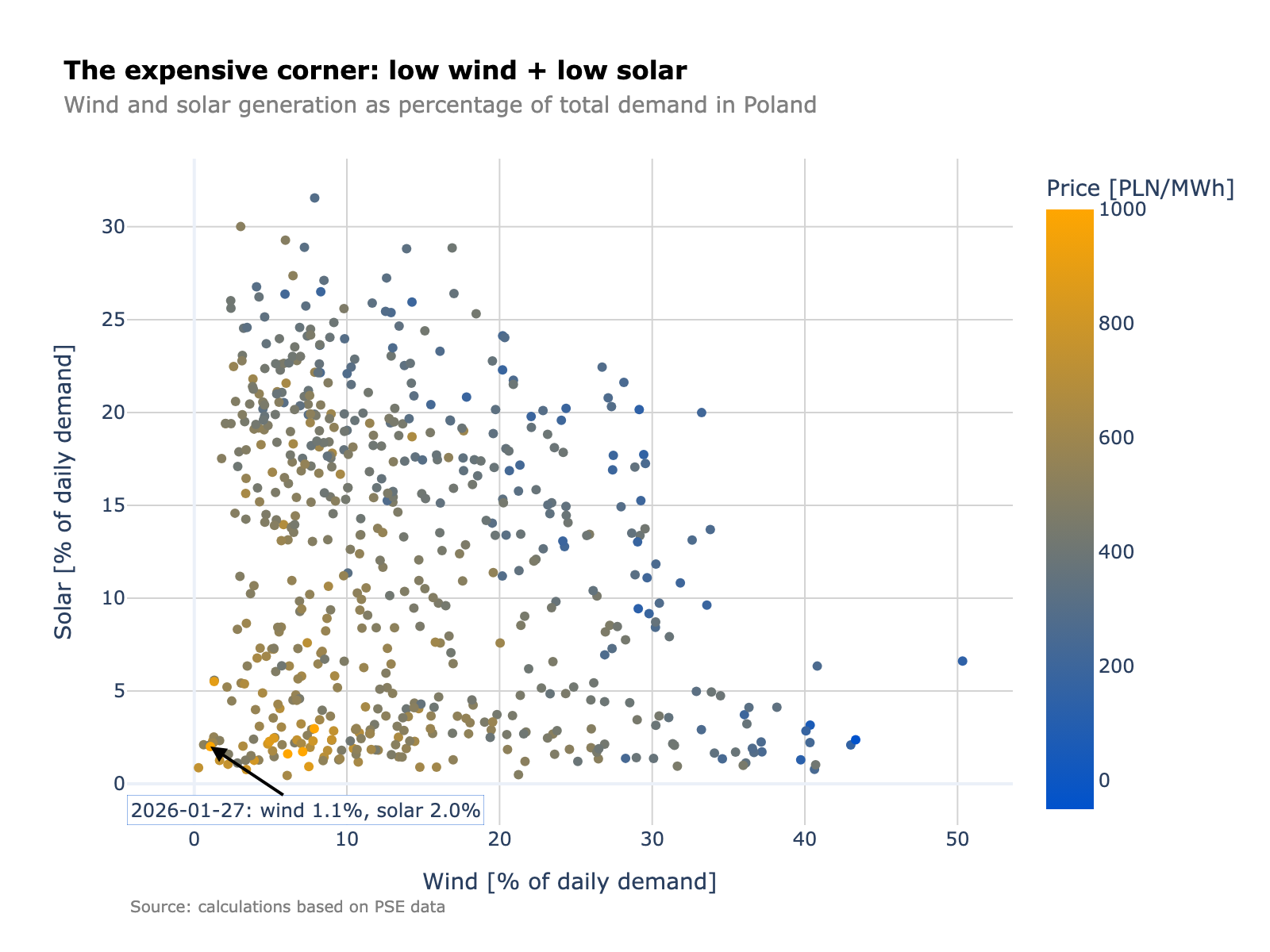

The rise of zero and negative prices

From 2024, a new feature appears at the low‑load end: more hours clear at zero or negative prices, and the trend line develops a visible downward bend around roughly 10 GW of residual load. Together, these points show that risk in the market has become two‑sided – very high prices when residual load is large and the system is tight, and very low or negative prices when residual load is small and inflexibility dominates. By 2025 this is no longer a curiosity but a regular operating condition, with more than 350 hours of negative prices already recorded.

Growing wind and solar push more hours into very low residual load territory. At the same time a large block of must‑run or low‑flex capacity (technical minima, CHP, long‑ramp thermal units) limits downward adjustment. When residual load sinks below this flexible threshold the clearing price has to fall — sometimes sharply negative — to force curtailment or stimulate exports.

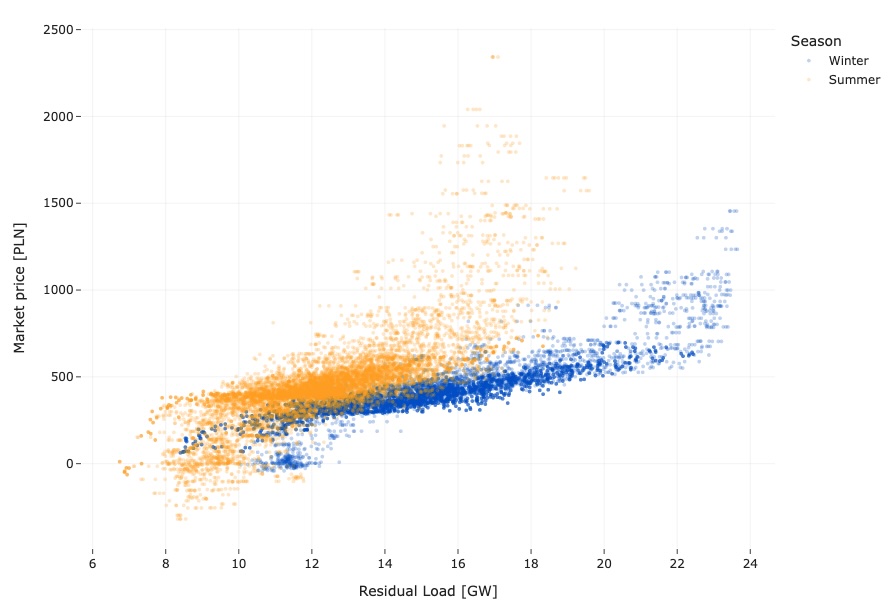

Seasonal view of residual load

Looking at the relationship by season adds another layer of detail. Winter operates over a wider residual‑load range (up to around 24 GW), while summer typically stays below 20 GW but delivers higher prices for the same residual load. Summer also shows more hours with negative prices and more extreme spikes, with a visibly steeper residual‑load/price slope.

Why this matters for “what-if” analysis

This evolving residual-load/price relationship is more than just a nice chart – it’s a practical tool.

If we can quantify the marginal sensitivity (PLN/MWh per GW) by season and hour, we can estimate renewable impacts (e.g. +2 GW PV deepening midday summer lows), value demand‑side shifts (lowering residual load in targeted blocks), and compare strategic portfolios: more batteries clipping peaks and possibly dampening low/negative episodes, or thermal fleet changes that alter steepness at high loads.

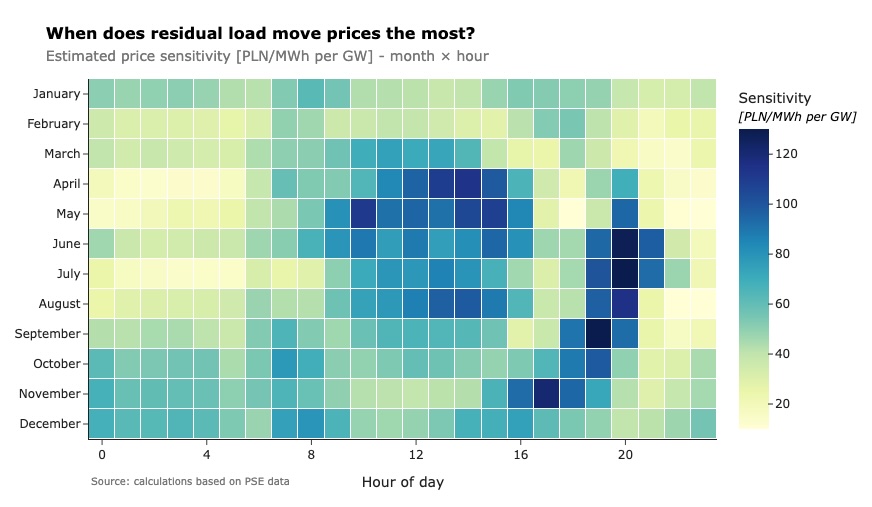

Residual-load price sensitivity: season and hour

To move from “what happened” to “what if”, we also need to know how much prices react to a small change in residual load at different times of the year and day. Here we map marginal price sensitivity (PLN/MWh change per 1 GW residual load shift) on a month × hour heatmap.

Looking at the heatmap, a few patterns stand out. Around the midday “solar dip” in residual load, even a small upward shift (less PV or a bit more demand) quickly pulls higher‑cost units onto the margin – the dark core in the middle of the plot. Put differently, a bit more solar generation in those hours quickly pushes prices down. At high demand in the morning and especially in the evening peak, sensitivity spikes again: extra residual load there steepens the curve fastest. By contrast, nights – particularly in summer – look relatively flat, with the stack fairly stable and prices much less sensitive to small changes in residual load.

The key insights is that the residual load impact is non‑linear: the more extreme the price level, the more sensitive it becomes to additional load. That convexity is the merit order in action — climbing the stack not only costs more per MW, the slope itself steepens at higher utilisation.

Implications.

A ±1 GW shift matters most in the midday trough and the evening peak; with rising RES penetration we expect those swing zones to widen and deepen. The sensitivity matrix also lets us compare +1 GW wind (flatter diurnal profile) vs +1 GW solar (midday‑heavy) and see how each reshapes the slope and volatility of the price curve.

From a business perspective, the heatmap shows when the market is most price‑sensitive to changes in residual load. That matters whenever new capacity is added or existing capacity is shifted, because those changes will move residual load and, in turn, reshape prices hour by hour. In rough terms, price change follows residual load change scaled by the sensitivity in each month and hour.

This has direct consequences for capture factors and revenues (you can read more about capture price dynamics in a separate post Poland’s solar generation boom and PV capture factors and in our live capture price dashboard). Adding solar or wind into hours with high sensitivity is more likely to drag prices down and compress capture prices, especially around the midday trough; adding into flatter parts of the heatmap has a softer effect on price levels and on realised revenues. The same logic applies to storage and demand response: shifting load away from high‑sensitivity hours, or discharging into them, can have an outsized impact on both price